Whether you’re a seasoned investor or just starting out, Adobe is a company that often stands out due to its strong market presence and innovative solutions. In this post, we’ll break down Adobe’s key financial metrics, business model, and valuation methods to help you determine whether Adobe is a worthwhile addition to your investment portfolio.

What’s in the News for Adobe?

Adobe recently made headlines with its Q3 earnings report. The company generated $5.4 billion in revenue, marking an 11% year-over-year increase, with earnings per share (EPS) rising to $11.85. Despite these strong numbers, Adobe’s stock saw a 9% dip after the earnings call. The market reaction suggests that investors might feel Adobe is currently overvalued, especially considering the competitive landscape and rising AI technologies.

CEO Shantanu Narayen emphasized the company’s “relentless innovation” as a key driver behind its success, but it’s clear the market has some reservations about Adobe’s future growth, which brings us to an in-depth analysis.

Adobe’s Fundamentals: A Closer Look

Adobe’s financials have long been a strong selling point for investors. Let’s break down some of the company’s key financial metrics:

- Average Revenue Growth: Adobe has a history of solid revenue growth. However, the company’s forecast for 2024 shows a projected slowdown, with expected growth at just 3%.

- PE Ratio: Currently, Adobe’s price-to-earnings (PE) ratio is around 46, slightly below its earlier value of 50 but still above the industry average of 41. This could indicate that Adobe is trading at a premium, particularly compared to its competitors.

- Profit Margins: Adobe boasts high gross profit margins of over 55%, thanks to its strong subscription model and product ecosystem.

- Free Cash Flow: Adobe’s cash flow remains stable, a key indicator of the company’s ability to reinvest and grow while maintaining profitability.

- Debt Coverage: Adobe has low long-term debt, and its free cash flow easily covers any liabilities, making the company financially secure.

Key Ratios That Matter

For investors, there are several critical ratios to watch when analyzing Adobe:

- Net Earnings Ratio: Adobe’s net profit margin stands at approximately 30%, a solid indicator of its operational efficiency and profitability.

- R&D ratio: Adobe has a stable 20% R&D ratio which might indicate a good competitive advantage. However, it is unclear where this money is spent and how it benefits the company.

Understanding Adobe’s Business Model

Adobe’s subscription-based business model has been the backbone of its success. The company’s Creative Cloud suite is a must-have for industries ranging from marketing to design, and its Document Cloud (featuring products like Adobe Acrobat) continues to be a market leader.

This recurring revenue model provides predictable cash flows, making Adobe a stable investment in the tech sector. However, the company is facing rising competition from AI-powered creative tools, which may pose a challenge to its market share moving forward.

Valuation Methods: How We Evaluate Adobe Stock

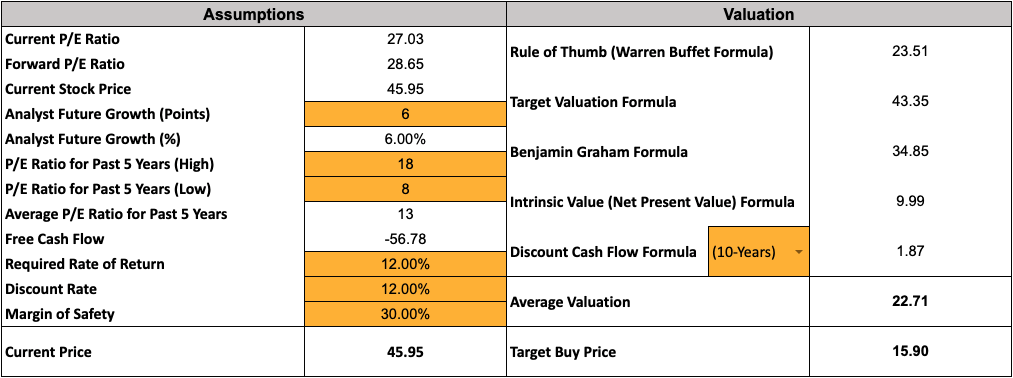

1. Discounted Cash Flow (DCF) Analysis

The discounted cash flow method estimates the present value of Adobe’s future cash flows, factoring in its efficiency and operational excellence. Here’s how we break it down:

- Projected Free Cash Flow Growth: We assume McDonald’s free cash flow growth will be 7% annually. This is a conservative estimate due to competition Adobe is facing with new AI softwares popping up. This figure is also in line with the past 5 years of revenue growth.

- Discount Rate: For DCF, we typically use a discount rate of 10%, which accounts for the risk of investing in individual stocks versus the broader market.

- Valuation: Based on the DCF model, McDonald’s intrinsic value is estimated at $80 per share.

2. Benjamin Graham’s Formula

The formula of Benjamin Graham mainly focusses on the growth rate and the company’s current EPS ratio. According to this formula, Adobe should be priced around $86.

3. Warren Buffett’s Rule of Thumb Formula

Similar to the Benjamin Graham Formula, the rule of thumb formula uses the same input however it undermines the 4.4% high yield bond rate that Benjamin included. Therefor this valuation is always slightly higher and prices the stock at around $118.

4. Target Valuation Formula

This formula emphasizes on the current EPS, an estimated P/E Ratio, growth rate and the period you are planning on holding the stock. This formula returned a valuation of $501

5. Intrinsic Value (NPV) Formula

This formula is a bit more elaborate and includes the cashflow, discount rate, number of periods, and residual value. This formula returned a price of $240.

Average valuation

Most statisticians know that the average is (almost) always right. Therefore, we are interested in what the average of all five formulas is. The average of all the formulas that we used is $205which is a lot higher than the price it is currently trading for ($536).

Now let’s dive deeper into the various valuation methods we use to assess whether McDonald’s stock is priced fairly.

Should You Invest in Adobe?

While Adobe remains a solid company with a strong business model, its current stock price appears to be higher than its intrinsic value based on multiple valuation methods. The growing competition from AI tools, coupled with a slowing growth rate, may raise concerns about whether Adobe can sustain its premium price.

If you’re a long-term investor with a focus on stable companies, Adobe could still be a good pick. However, waiting for the stock to come closer to its intrinsic value might be a more prudent strategy.

Conclusion

Adobe is a market leader with impressive financials and a subscription model that ensures stable cash flow. However, based on our analysis, the stock appears to be overvalued at current prices. Keeping Adobe on your watchlist and waiting for a better entry point could be the best move for value-focused investors.

As always, do your own research and consider your investment strategy before making any decisions.